August 20, 2025Expert Insights

Brazil’s Fintech Revolution Built Access at Scale. Now It Faces the Cost of Speed

Brazil has become the most important laboratory for digital finance in Latin America – perhaps the world. In just four years, Pix turned Brazil into a cashless pioneer – but also a testing ground for cybercrime tactics. What happens when 150 million people are brought online before the guardrails are built?

The same speed that built inclusion has now accelerated its risks. In this crucible of progress, systemic threats have begun to emerge.

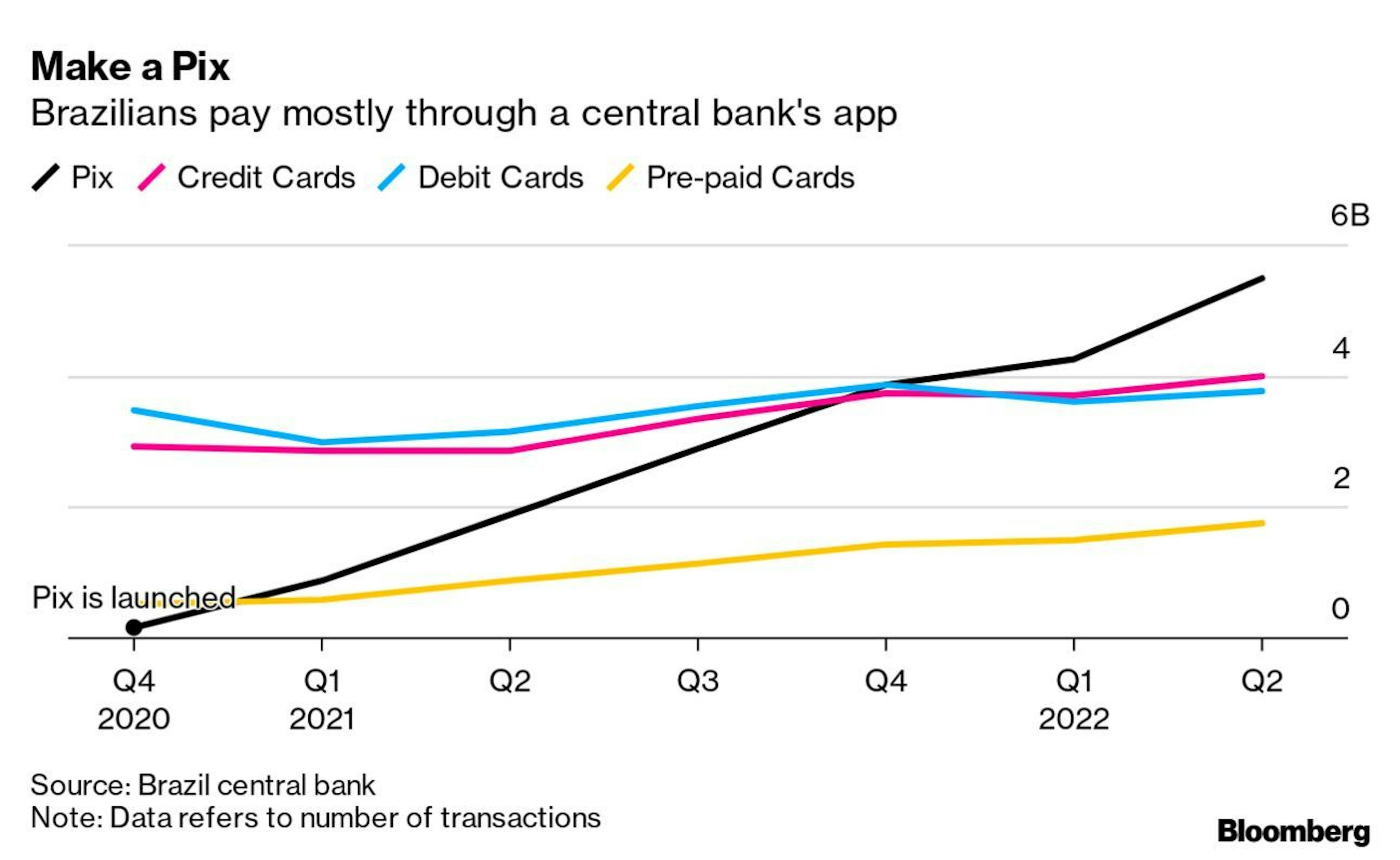

In late 2020, the Central Bank of Brazil launched Pix. More than an instant payment system, it became a public utility for digital life – and an alternative to global payment systems. By the end of 2024, 156 million people and over 15 million businesses were using Pix. It processed nearly 68.7 billion transactions that year – worth close to $5 trillion. That’s more than the country’s entire GDP.

Pix replaced cash, overtook debit cards, and reshaped everyday financial behavior. It also gave fintechs a seamless way to build products on top of real-time rails. Public infrastructure created a private innovation boom.

Between 2017 and 2024, Brazil cut its unbanked population by more than half. Today, over 84% of adults have access to a bank account. But this inclusion is often shallow. Many first-time users entered the system not by choice, but through necessity – like during the pandemic, when government emergency aid drove millions to open digital accounts.

Neobanks like Nubank (105M users), Mercado Pago (50M), and PicPay (36M) surged in adoption. But access to digital finance is only the first step. Financial literacy and resilience have lagged behind.

Wherever there is digital scale, fraud follows. Brazil is now facing an epidemic of cybercrime. The same frictionless tools that powered inclusion are now being exploited by professionalized fraud networks.

Criminal groups have moved from the streets to the screen. Fraud cases quadrupled between 2018 and 2023, while physical robberies dropped. Fraud is now Brazil’s most common property crime.

Probably every Brazilian can share a story about themselves – or someone they know – being a target of a financial scam.

The methods are getting increasingly sophisticated. Deepfake audio scams, fake bank call centers, and cloned WhatsApp accounts now operate at industrial scale. Organized crime has discovered that digital fraud offers lower risk and higher return than traditional crime.

Access to credit has been another hallmark of Brazil’s fintech revolution. But it has created a paradox: as more people gain access to loans, many fall into unmanageable debt. The culture of borrowing outpaced the culture of planning.

The term "superendividamento" – over-indebtedness that threatens basic subsistence – has entered public policy. The 2021 Over-Indebtedness Law (Lei do Superendividamento) to protect vulnerable borrowers and preserve their "mínimo existencial" (essential income). But enforcement has struggled to keep pace with market forces.

Brazil’s digital transformation has achieved scale – but now faces a sustainability test. To preserve the benefits of financial innovation while reducing systemic risk, stakeholders must act on four fronts:

Brazil’s leadership in digital finance is clear. The next step is ensuring it can last – securely, responsibly, and at scale.

Brazil’s case is not unique. Other countries embracing rapid digitalization will likely encounter the same tensions: between access and risk, between scale and trust.

The Brazilian experience underscores some strategic imperatives:

Brazil's digital journey has been bold, fast, and largely successful. But it now stands at a crossroads. Either the ecosystem evolves toward sustainable, secure, and inclusive growth – or it risks eroding the very trust that made its transformation possible.

What was meant to be the decade’s greatest achievement – digital credit in just a few clicks, 24/7, for any Brazilian with a device – has become fertile ground for fraudsters. In the rush to “release instant credit,” we skipped validation layers and outsourced the risk to the user’s good faith.

In that gap between convenience and carelessness, scams flourished.

Today, fraud no longer appears at the cashier’s desk. It hides in code, rooted devices, masked VPNs, and the superhuman cadence of bots. Each field removed from an onboarding form opens another point of vulnerability.

That’s where solutions like JuicyScore become essential. Detecting, in milliseconds, a newly created domain, an intercontinental IP jump, or the invisible root of an Android device is not a luxury — it’s the cost of ensuring that the dream of inclusive credit doesn’t turn into a nightmare, for both customers and those carrying the risk on their balance sheets.

Democratizing credit remains vital to Brazil’s future – but it will only be sustainable when built on an invisible layer of trust. The past few years have proven what’s achievable. The priority now is to invest in resilient structures that endure.

An expert article by JuicyScore's Business Development Manager, featuring first-hand insights on fintech expansion in Latin America. Discover how digital signals and device intelligence are redefining risk assessment in high-fraud environments.

Fraud monitoring stands as a Fintech watchman against the ever-evolving fraudsters’ tactics. Particularly for fintech businesses, the stakes are sky-high. With the rapid pace of innovation, digitalization, and the interconnected nature of financial services, the challenges are fiercer.

Modern technologies are becoming more robust, and security measures more sophisticated. But there’s one vulnerability that can’t be patched — human trust.

Get a live session with our specialist who will show how your business can detect fraud attempts in real time.

Learn how unique device fingerprints help you link returning users and separate real customers from fraudsters.

Get insights into the main fraud tactics targeting your market — and see how to block them.

Phone:+971 50 371 9151

Email:sales@juicyscore.ai

Our dedicated experts will reach out to you promptly