Fraud Detection for Digital Banking & Online Lending

JuicyScore helps digital banks and lenders detect synthetic identities, prevent account takeovers, and assess risk without personal data. Behavioral analytics and device intelligence make it easy to stop fraud early — before disbursement, onboarding errors, or compliance issues happen.

Book a Demo

Leaders Grow with JuicyScore

Detect Fraud Before the Loan Is Issued

Fraud risk often appears at the application stage — through fake accounts, duplicate identities, or manipulated devices. Traditional scoring and document checks miss these signals. JuicyScore enables real-time decisions using device fingerprinting and behavioral risk profiles — helping you block high-risk borrowers, detect multi-accounting, and reduce default rates. All without adding friction for trusted users.

Streamline Onboarding, Strengthen Security

Identify synthetic identities and linked devices with high accuracy

Identify synthetic identities and linked devices with high accuracy- Prevent account takeovers using real-time behavioral signals

- Cut friction with adaptive scoring based on device-level risk

- Monitor for VPN usage, device tampering, and session anomalies

- Improve portfolio performance while staying compliant

Learn How It Works

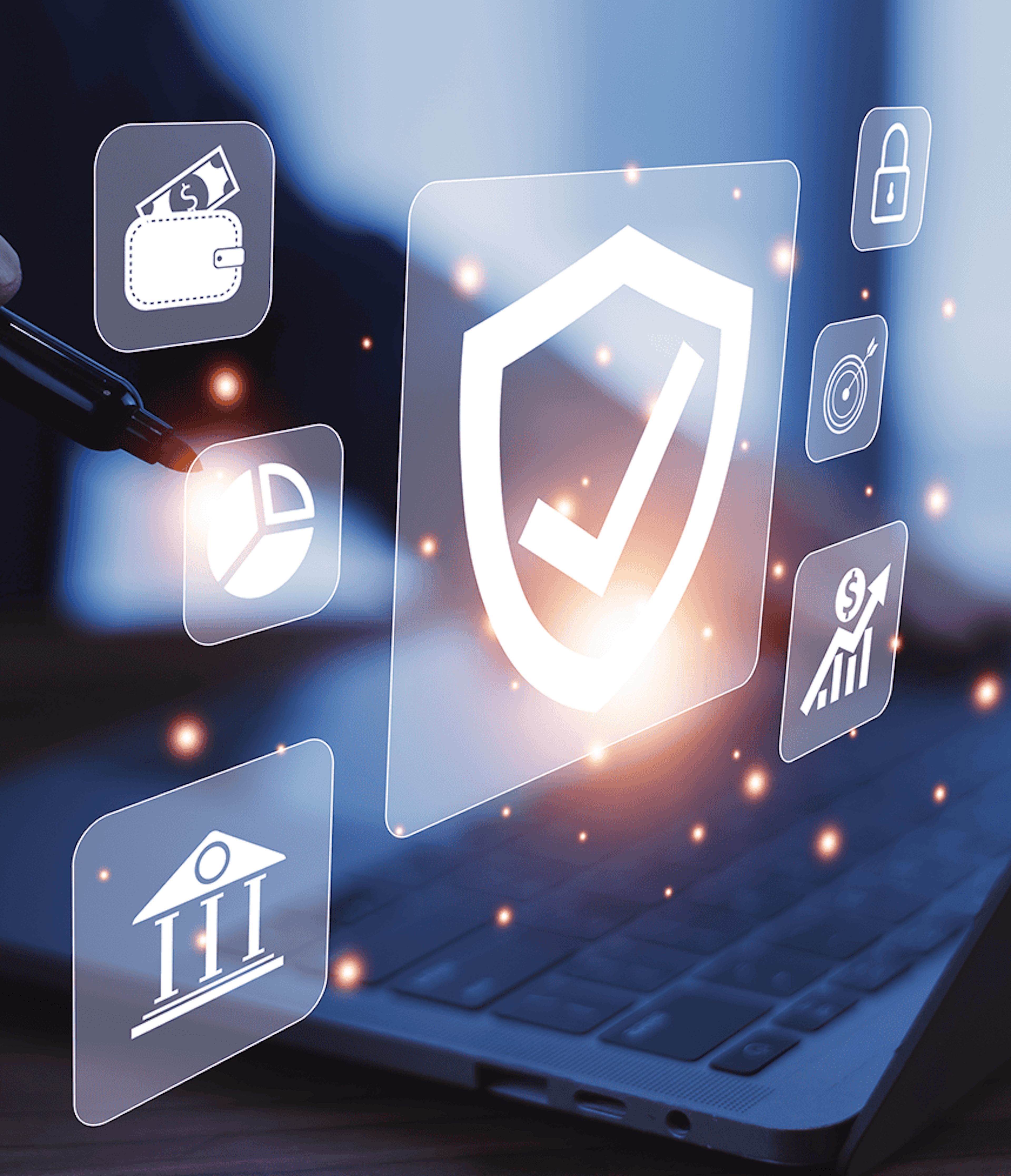

Utilizing over 65,000 data points, JuicyScore generates highly predictive risk score models to detect fraud and assess risk in real time. Our output data vector includes device intelligence, user behavioral patterns, internet connection insights, and software data for precise decision-making. Protect your business with advanced fraud prevention while ensuring a seamless customer experience.

Learn more

Our Clients’ Success Stories

Related Articles

See How We Spot Fraud Before It Happens — Book Your Expert Session

See It in Action with a Real Expert

Get a live session with our specialist who will show how your business can detect fraud attempts in real time.

Explore Real Device Insights in Action

Learn how unique device fingerprints help you link returning users and separate real customers from fraudsters.

Understand Common Fraud Scenarios

Get insights into the main fraud tactics targeting your market — and see how to block them.

Our Contacts:

Phone:+971 50 371 9151

Email:sales@juicyscore.ai

Leading Brands Trust JuicyScore:

Get in touch with us

Our dedicated experts will reach out to you promptly