October 7, 2025Expert Insights

RBI’s 2025 Authentication Mandate: Why Device-Level Intelligence Is Now Critical

The Reserve Bank of India is not simply introducing new rules – it is reshaping the entire authentication paradigm. By steering India beyond OTPs, the RBI is weaving in risk-based and alternative methods as the new standard for digital payments security. The country is moving rapidly toward dynamic, intelligence-driven authentication. For banks and payment providers, this is both a compliance challenge and a strategic opportunity: those who adopt risk-based authentication early will not only fortify defenses against fraud, but also gain a decisive edge in earning customer trust and loyalty.

In early 2025, the Reserve Bank of India (RBI) released a circular on payments security and authentication, setting out requirements that come into force by April 2026. The regulator’s message is clear: static two-factor authentication (2FA), particularly SMS-based OTPs, is no longer sufficient to protect India’s fast-growing digital payments ecosystem. Instead, RBI encourages issuers and payment providers to adopt risk-based authentication – adding behavioral, location, and historical intelligence to security checks.

For over a decade, SMS-based OTPs have been the default second factor for online payments in India. But with the surge of phishing, smishing, and vishing attacks, OTPs face growing challenges. Fraudsters can trick users into sharing codes or hijack them through malware and SIM swap fraud. With UPI and card transactions reaching billions each month, a static credential like OTP cannot keep up with the speed and sophistication of today’s fraud.

Risk-based authentication (RBA) is not about adding more friction to every payment. Instead, it means evaluating each transaction in real time: is this behavior consistent with the customer’s history? Is the device location typical? Does the device itself appear trustworthy? If the risk is low, the transaction proceeds seamlessly. If the risk is high, additional checks are applied. This adaptive approach balances fraud prevention with smooth customer experience.

To make RBA effective, institutions need strong data signals beyond OTP. This is where device intelligence plays a key role. Device-based risk models can combine behavioral biometrics, location consistency, and historical transaction patterns — without relying on sensitive personal data. This helps issuers distinguish between genuine users and fraud attempts, even when fraudsters spoof browsers, use emulators, or recycle stolen identities.

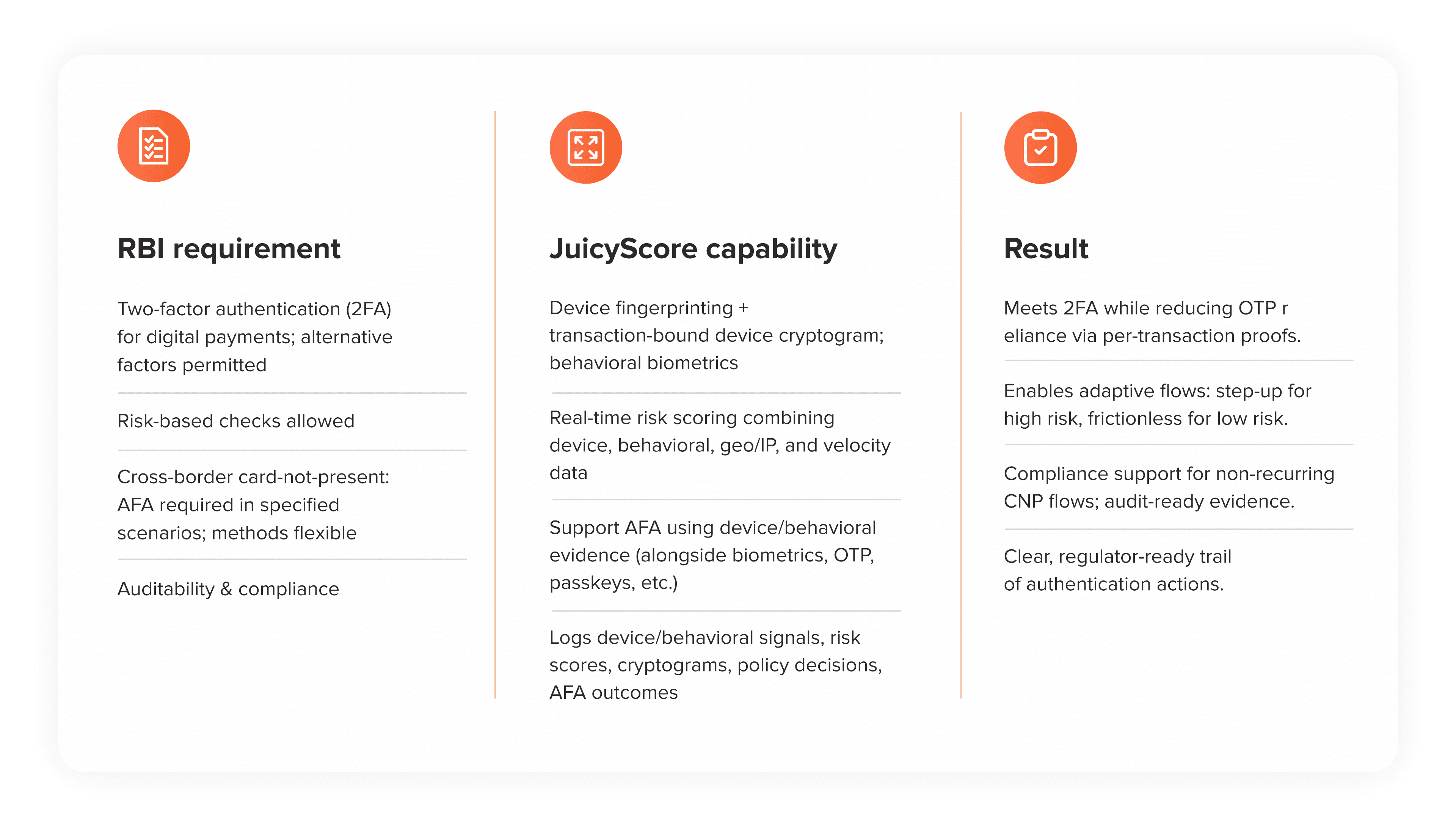

JuicyScore’s platform is designed to align with RBI’s April 2026 requirements:

This approach delivers regulator-ready evidence (transaction ID, device hash, cryptogram, risk score, applied policy, AFA outcome), lower OTP dependency, support for cross-border CNP scenarios, and privacy-by-design practices aligned with DPDP.

For banks, NBFCs, and payment providers, the April 2026 deadline leaves limited time for preparation. Compliance requires building a truly adaptive fraud prevention framework that can scale with India’s digital economy. Those who act early, investing in device intelligence and behavioral analytics, will not only meet regulatory expectations but also reduce fraud losses, improve approval rates, and protect customer trust.

RBI’s stance reflects a global shift: regulators and industry leaders alike are moving away from static controls toward dynamic, intelligence-driven authentication. For India, where digital payments volumes are unmatched, the move to risk-based authentication is not just compliance — it’s a necessity to sustain growth, inclusion, and security at scale.

By explicitly mandating risk-based authentication, India is positioning itself among the first major markets to embed behavioral, location, and device intelligence into payment security standards. Few regulators worldwide explicitly advocate for a risk-based approach instead of simply strengthening outdated static methods. For India, this shift is crucial: UPI alone processes more than 18 billion transactions per month — volumes that rival or exceed those of the EU or US. RBI is signaling that the future of payments security lies in real-time, data-driven assessment rather than static controls.

JuicyScore Mumbai Event Spotlights: Digital Fraud Trends

Manish Thakwani shares expert insights on PII-free risk scoring in India’s DPDP era — why device intelligence is key to compliance, fraud prevention, and growth.

Trends of remote access and social engineering risk prevention in 2024

Get a live session with our specialist who will show how your business can detect fraud attempts in real time.

Learn how unique device fingerprints help you link returning users and separate real customers from fraudsters.

Get insights into the main fraud tactics targeting your market — and see how to block them.

Phone:+971 50 371 9151

Email:sales@juicyscore.ai

Our dedicated experts will reach out to you promptly